Climate Policy

climate-policy

4 min. read

Key takeaways

GHG Protocol and SBTi are releasing major updates in 2027, tightening requirements for emissions data quality, boundary-setting, and mitigation practices.

Companies will face higher expectations for scope 2 precision, scope 3 traceability, and transparent target-setting, raising the bar for credible climate action.

These changes reflect expectations already present in investor pressure and regulatory proposals.

Don’t wait for 2027. Businesses should act now to evaluate data systems, supplier relationships, and climate targets in anticipation of these new standards.

Why are GHG Protocol and SBTi updating?

Major updates to the Greenhouse Gas Protocol (GHG Protocol) and the Science Based Targets initiative (SBTi) are on the horizon, with adoption expected by 2027. These changes mark a critical moment for companies to evaluate how they measure, report, and act on greenhouse gas (GHG) emissions. Many companies will find it challenging to meet the data quality, traceability, and supplier engagement requirements in these updates.

Why do these updates matter now?

The urgency of climate change is becoming more and more apparent, with recent assessments showing that warming is likely to exceed the 1.5° C target within five years. Rapid regulatory shifts in Europe, the US, and elsewhere are pushing climate disclosures forward. These frameworks are evolving to:

Reflect improved data availability

Improve the credibility of climate claims

Clarify acceptable mitigation pathways

“A decade ago, many things were unmeasurable that we can measure today,” says Dr. Colin McCormick. “We now have hourly grid data, product-level emissions, and better traceability across supply chains.”

These advancements are directly informing the revisions to both frameworks.

Understanding the role of GHG Protocol and SBTi in climate reporting

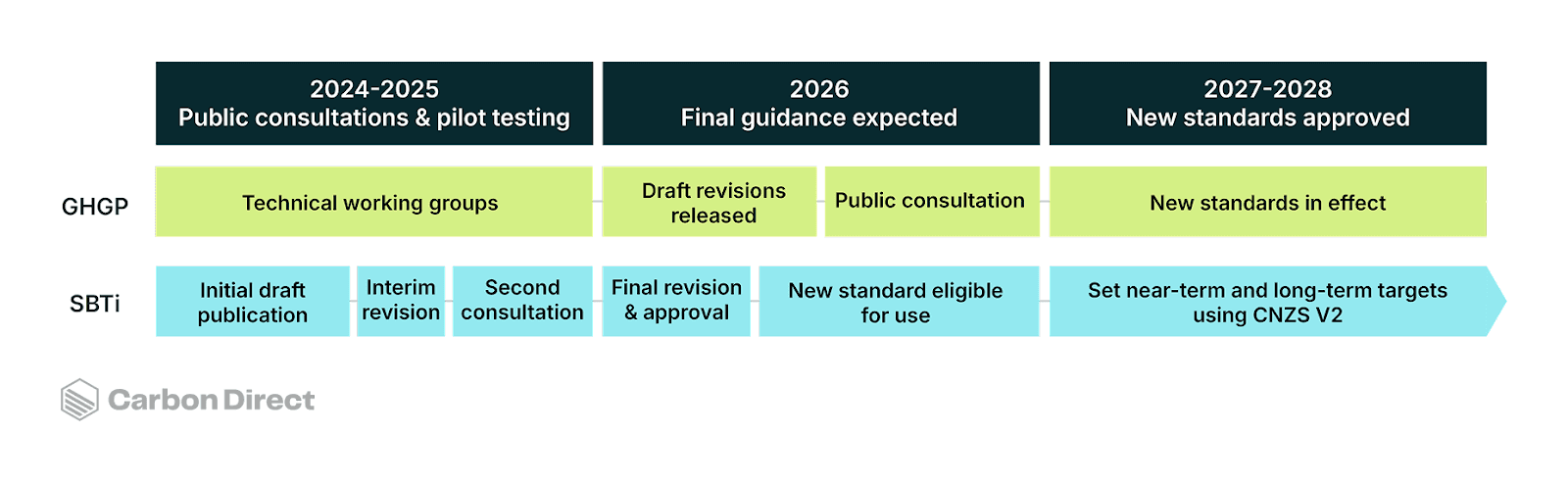

The GHG Protocol is the global standard for calculating and reporting corporate emissions. It underpins climate reporting across frameworks like CDP and the International Sustainability Standards Board (ISSB), and regulations such as the Corporate Sustainability Reporting Directive (CSRD) and California SB 253. Many parts of the GHG Protocol are under review, including the Corporate Accounting and Reporting Standard, the Scope 2 Guidance, and the Scope 3 Standard. The scope 2 public consultation period opened in October 2025 and runs through January 2026.

SBTi defines how companies align their emissions targets with the Paris Agreement, primarily through its flagship Corporate Net Zero Standard (CNZS). SBTi is currently developing Version 2 of CNZS. The first draft was released in April 2025, followed by a revised draft in November 2025 and a public consultation period that was open through December 12, 2025.

Final standards for both the Scope 2 Guidance and CNZS are expected in 2027.

The SBTi defines how companies align their emissions targets with the Paris Agreement. The draft Corporate Net Zero Standard (CNZS) Version 2.0 was released in April 2025.

Both are undergoing revisions through public consultations and expert working groups, with final guidance expected in 2027.

GHG Protocol updates: What’s changing for scope 2 and 3

Companies should prepare for fundamental changes to how indirect emissions are measured and reported. As Dr. McCormick explains, the GHG Protocol is shifting toward “greater precision and operational relevance” addressing long-standing challenges like spend-based scope 3 data and annual averages in scope 2 electricity use.

Key proposed scope 2 changes:

Shift from annual to hourly location-based measurement

Regional and temporal constraints for use of renewable energy certificates (RECs)

Hierarchy of emission factors and introduction of load profiles

Supplemental consequential method using marginal emissions data

Key proposed scope 3 changes:

Mandatory reporting of significant emissions categories (above a 5% threshold)

Disaggregation of spend-based vs. activity-based data

Increased supplier engagement and multi-year data quality plans

“These changes aim for precision,” says Dr. McCormick. “It’s not just about accuracy, it’s about making emissions data operationally relevant instead of relying on broad averages.”

SBTi Version 2.0: What’s new for climate targets and mitigation

SBTi’s proposed CNZS Version 2.0 introduces updates designed to increase ambition and accountability, while improving practical implementation. Dr. Meera Atreya emphasizes the growing urgency: “The remaining budget of greenhouse gases we can emit without compromising our climate goals is shrinking and that’s making the science-based piece more difficult every day.”

Proposed target setting updates:

Separate scope 1 and scope 2 targets, instead of a combined target

Required location-based scope 2 targets and optional low-carbon electricity targets

Increased flexibility for scope 3 targets with options based on materiality, ability to influence or control, or emissions intensity

Transition to a cyclical target validation model, requiring companies to explain deviations from progress towards achieving previously approved targets

Proposed mitigation guidance:

Recognition of indirect mitigation tools (e.g., related to SAF, low-carbon materials)¹

Procurement of goods, services, and market-based instruments from applicable activity pools

Shift from national or regional REC matching to grid-specific matching

Required data traceability improvements over time

Recognition of near-term actions to support mitigation beyond the value chain (e.g., through carbon removal purchases)

Mandatory carbon removal purchasing requirements prior to the net-zero year

“This version raises the bar,” says Dr. Atreya. “It creates real accountability while recognizing the complexity of value chain emissions.”

Implementation timeline

2024–2025: Public consultations and pilot testing

2026: Final guidance expected, with the new standards eligible for use

2027: New standards approved, taking effect in 2028 or later

What can companies do now to prepare?

These updates will require a significant lift that companies need to prepare for. Waiting increases the risk of falling behind on compliance, transparency, and investor expectations. Start now to strengthen the internal systems, supplier relationships, and data quality needed to meet the upcoming standards.

Upgrade your emissions data systems

Assess whether you can track scope 2 emissions hourly and by region.

Begin analyzing granular electricity data alongside annual averages.

Identify infrastructure gaps and evaluate software or partners to support new data requirements.

Pressure test your scope 3 approach

Review how much of your scope 3 footprint uses spend-based estimates.

Map out where activity-based or supplier-specific data could replace spend.

Develop a multi-year data improvement plan for your value chain.

Initiate supplier engagement

Identify your highest-emitting suppliers or categories and open a dialogue.

Standardize data requests and offer support where possible.

Adopt a phased approach based on supplier maturity.

Revisit your climate targets

Ensure your targets account for scope 1 and scope 2 emissions separately.

Check whether your current boundaries cover all material emissions categories.

Model how your targets may need to shift under the new rules.

Addressing these areas early will reduce audit risk, improve transparency, and position your company as a credible climate leader as standards evolve.

Why early action gives companies a competitive edge

“Companies that wait could find themselves far behind on both compliance and credibility,” Dr. Atreya warns. In contrast, early movers can:

Improve data systems and internal alignment

Build supplier readiness

Evaluate procurement of high-quality removals and RECs

Pressure test targets against evolving standards

How can Carbon Direct help?

Not sure where to start? Don’t wait until 2027. Get expert support today.

Carbon Direct provides science-backed guidance to help organizations stay ahead:

Carbon accounting aligned with GHG Protocol updates

Supplier engagement to build scope 3 traceability

Science-based target setting under SBTi’s evolving standards

Identify direct and indirect decarbonization levers to accelerate progress toward targets

Carbon credit diligence using proprietary quality criteria

Our scientists and advisors partner with clients to design credible, actionable climate strategies tailored to your operations.

Contact us to get started.

1 - This applies when traceability either to the specific emissions source or the activity pool cannot currently be established, or if insurmountable barriers persist in addressing a source of emissions.